For most of modern market history, options were tools used primarily for hedging and positioning around longer-term views. Traders bought contracts weeks or months out, institutions used them to protect portfolios, and volatility moved at a pace that reflected macro changes.

That structure has changed dramatically over the last few years.

Today, a large portion of the options market revolves around instruments that expire the same day they are traded. These contracts are called 0DTE options - Zero Days to Expiry.

And they are quietly changing how markets move.

The Explosion of Same-Day Options

Just a few years ago, same-day options were barely a category.

Today they dominate index options trading.

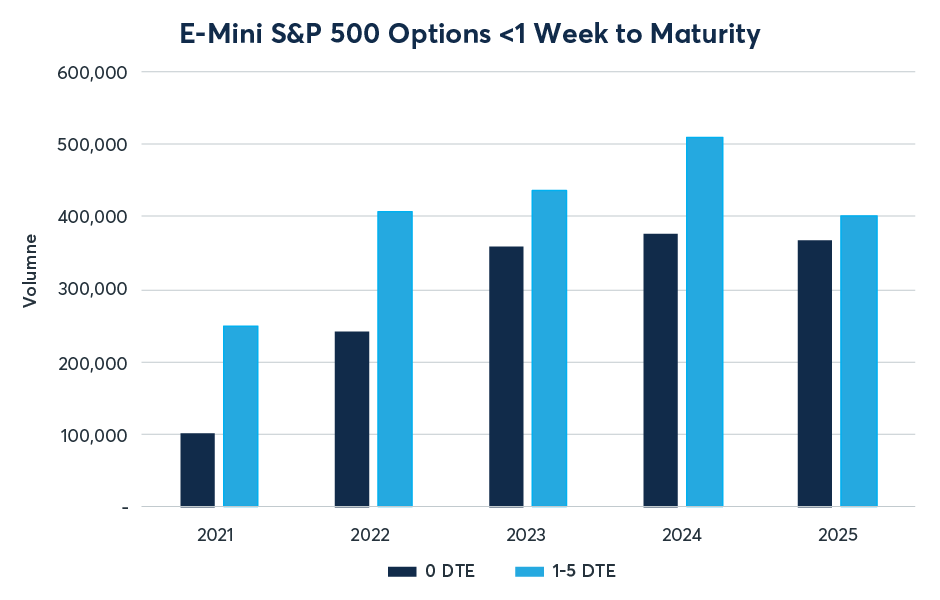

Data from the CME Group shows how quickly short-dated options have grown. Four years ago, options with 0–5 days to expiry in E-mini S&P 500 contracts averaged around 350,000 contracts daily, while 0DTE volumes alone grew from roughly 100,000 to around 370,000 contracts in that period.

That is not a marginal shift.

That is a structural change in how traders interact with markets.

Source: CME Group

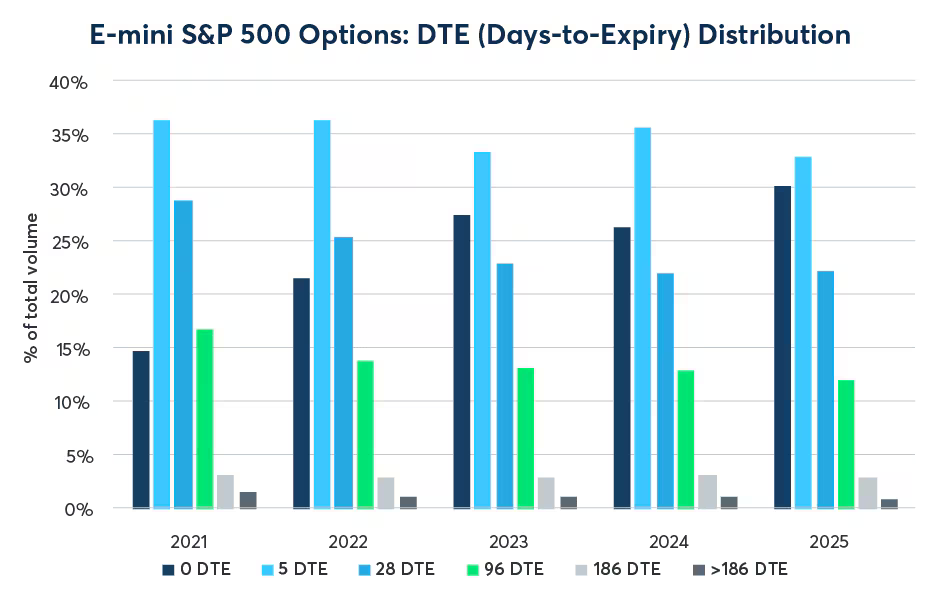

Source: CME Group

The attraction is obvious. These options are cheap, fast-moving, and extremely sensitive to price movements. Because they expire within hours, traders quickly find out whether they were right or wrong.

But focusing only on the payoff misses the bigger story.

The real story is how this flow influences the market itself.

Why Traders Love Short-Dated Options

There is a reason these instruments exploded in popularity.

Short-dated options offer a few structural advantages:

Lower premium

Because there is very little time until expiration, the option’s price is relatively cheap. Traders can gain exposure with less capital.

Precision around events

Short-dated options allow traders to target specific events like central-bank decisions, economic data releases, or geopolitical announcements.

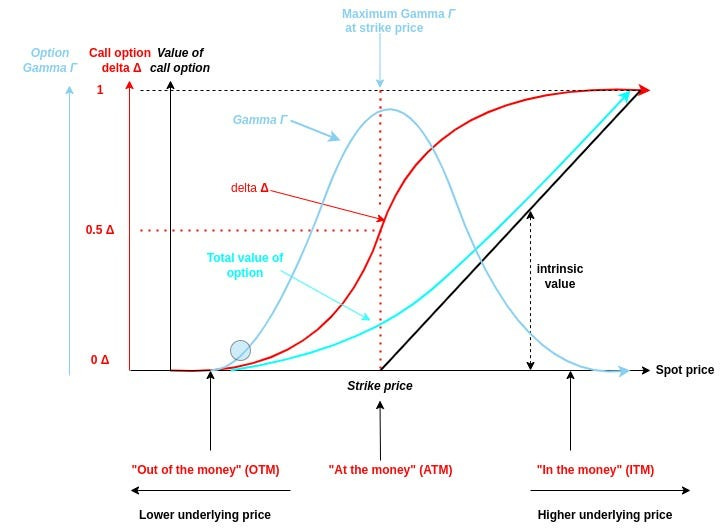

Higher gamma sensitivity

As expiration approaches, an option’s sensitivity to price movement increases dramatically. This means small price moves can produce large changes in the option’s value.

For institutions, this makes them powerful risk-management tools.

For example, CME describes how traders may use weekly options to position around macro data such as GDP releases, unemployment reports, or central-bank announcements.

This allows investors to isolate risk to a specific event without holding longer-dated positions.

A Real Example: Trading Around Economic Data

Imagine a trader expecting oil prices to rise after strong manufacturing data.

Manufacturing activity is closely linked to energy demand. A higher reading in the ISM Manufacturing Index often signals stronger industrial activity and potentially higher oil consumption.

CME provides a simple example of how traders might structure a bull call spread in WTI crude oil weekly options to capture a moderate move.

If oil futures are trading at $70, a trader might:

• Buy a $71 call

• Sell a $74 call

If the data surprises to the upside and oil rises to $73, the trade profits while limiting downside risk.

This is a classic use of short-dated options: expressing a view around a specific market catalyst.

The Hidden Market Mechanics

But there is another layer most traders never see.

Whenever someone buys an option, someone else must sell it.

Often that seller is a market maker.

Market makers usually hedge their exposure in the underlying asset. If traders buy calls, the dealer may hedge by buying the underlying futures or index. If traders buy puts, the dealer may hedge by selling.

With long-dated options this happens gradually.

With 0DTE options, it happens extremely fast.

Because these options are so close to expiration, they have very high gamma - meaning small price changes force dealers to adjust their hedges aggressively.

Dealer hedging activity can amplify market moves when short-dated options dominate trading.

This creates a feedback loop where price movements trigger hedging flows, and those hedging flows can move the market further.

That’s one reason why intraday markets sometimes feel unusually mechanical.

A Market Built for Stimulation

There is also a behavioral dimension to all of this.

Short-dated options compress the entire trading experience into a few hours.

Trade → result → repeat.

Fast outcomes create powerful psychological feedback. Wins and losses arrive quickly. The temptation to re-enter immediately is strong.

Daily options exist partly because markets demand precision and event-driven hedging.

But they also exist because traders crave speed and intensity.

And the faster the feedback loop becomes, the easier it is to confuse activity with edge.

The Bigger Structural Shift

The rise of short-dated options reflects something deeper about modern markets.

Risk is increasingly event-driven.

Central-bank announcements. Inflation data. Elections. Supply shocks. Geopolitical events.

These catalysts can move markets within minutes.

Short-dated options give traders the ability to isolate that risk precisely, which is why institutions use them for tactical hedging.

But they also introduce new dynamics into price behavior.

Flows matter. Hedging matters. Positioning matters.

The modern market is not just reacting to news.

It is reacting to derivatives positioning reacting to price.

The Discipline Problem

Short-dated options themselves are not inherently dangerous.

In professional hands they are tools for precision.

But when used without structure, they can easily become instruments of overtrading.

Fast instruments amplify emotional decisions.

That is why performance tracking matters so much in modern markets. When traders analyze patterns - trade frequency, risk escalation after wins, clustering of losses - they often discover that their largest drawdowns coincide with their most active periods.

The instrument is rarely the problem.

The absence of discipline is.

Markets Are Evolving

The market structure traders face today is very different from the one that existed ten years ago.

Algorithmic flows dominate liquidity. Prediction markets are emerging as probability signals. And short-dated options are reshaping intraday volatility.

Understanding price alone is no longer enough.

The edge increasingly belongs to traders who understand the mechanics behind price movements.

Because sometimes the market is not moving because of new information.

Sometimes it is moving because the options market forced it to.