Most traders spend about 6.5 hours a day watching the market. Charts open, candles forming every minute, prices ticking up and down while traders analyze patterns and search for opportunities. It’s easy to assume that this is where most of the market’s value is created — during the hours when everyone is actively watching and trading.

But what if the market does most of its work when nobody is watching?

That question led me to analyze every single trading day of the NIFTY 50 index from 1999 to 2025. Instead of treating each trading day as one continuous return, I split it into two separate components. The first was the overnight return, measured from the previous day’s close to the next day’s open. The second was the intraday return, measured from the market open to the market close on the same day.

In simple terms, this allowed me to separate what happens while the market is closed from what happens while traders are actively trading.

The results were surprising.

Most of the Market’s Gains Happened Overnight

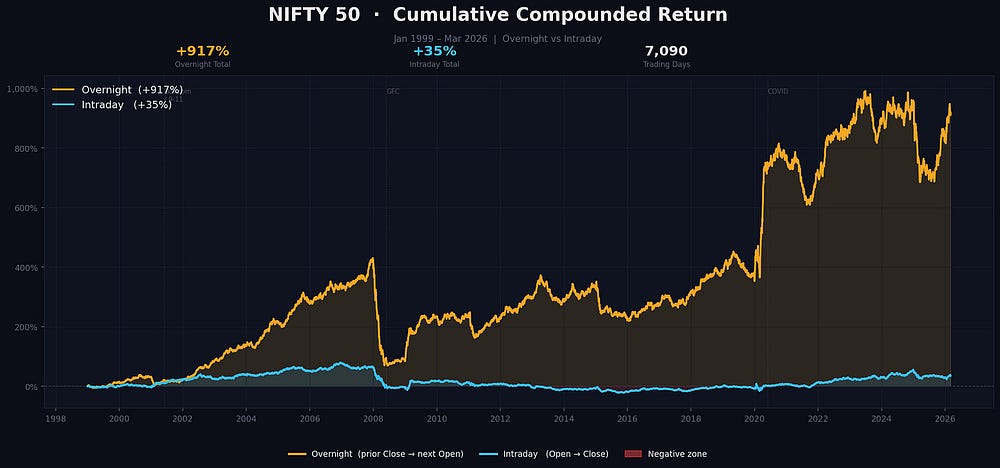

When the returns were compounded over the full 26-year period, a striking pattern emerged. The vast majority of NIFTY’s long-term gains came from overnight price movements, not from intraday trading.

Over the entire dataset, the cumulative overnight return reached roughly +917%, while intraday returns contributed only about +35%. The difference is not small — it fundamentally changes how we think about where returns are generated in the market.

If you removed overnight price movements entirely and only captured intraday returns, the long-term growth of the index would look dramatically different. The bulk of compounding that investors experienced over the past quarter century occurred between sessions, during the hours when markets were closed.

This is visible in the chart below, which separates cumulative returns into overnight and intraday components.

What stands out immediately is how steadily the overnight component drives the long-term growth of the index, while the intraday component remains relatively flat for extended periods.

The Pattern Survives Every Market Cycle

One obvious question is whether this result is driven by a specific market period. Perhaps it only occurred during one particular bull run or crisis.

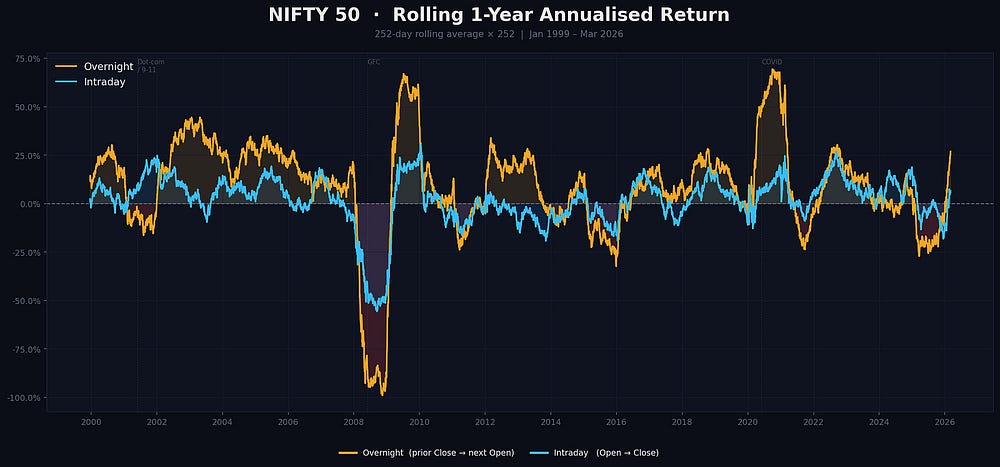

But when the data is examined across different market regimes, the pattern remains remarkably consistent. The dataset spans the dot-com aftermath, the global financial crisis of 2008, the COVID crash and recovery, and multiple bull and bear cycles. Despite these dramatic shifts in market conditions, the long-run contribution of overnight returns continues to dominate.

This becomes even clearer when looking at rolling one-year returns. Intraday performance fluctuates significantly, frequently moving between positive and negative territory. Overnight returns, however, tend to contribute the majority of positive compounding over time.

For long stretches of time, intraday returns were either flat or negative, while the overall market continued to rise due to gains that occurred outside trading hours.

This phenomenon is not unique to India. Academic research has documented similar patterns across many global equity markets, including U.S., European, and Asian indices. In quantitative finance, this is sometimes referred to as the “overnight drift anomaly.”

Annual Returns Tell the Same Story

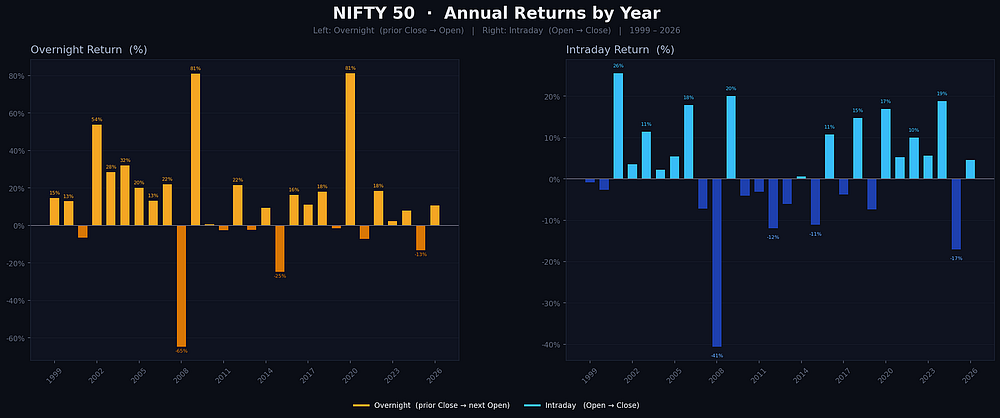

To further understand how this plays out in individual years, the data can also be broken down into annual overnight and intraday returns.

When the yearly performance is separated, the pattern becomes even more visible. In many years, the overnight component captures the majority of positive performance, while intraday returns often contribute relatively little or even turn negative.

Even during periods of strong bull markets, the data suggests that the index frequently does most of its upward movement through overnight gaps rather than sustained intraday trends.

There are several structural reasons why so much price discovery occurs between

Why Markets Move More Outside Trading Hours

There are several structural reasons why so much price discovery occurs between sessions.

The first is that important information often arrives when markets are closed. Corporate earnings announcements, regulatory decisions, macroeconomic data releases, and geopolitical developments frequently occur outside trading hours. When markets reopen, prices immediately adjust to reflect this new information.

Second, global market transmission plays a major role. Indian markets open after major overnight developments in the United States and Europe. Movements in global equity indices, commodity prices, and currency markets during the night often influence the opening price of NIFTY.

Third, institutional positioning can occur outside regular market hours through futures markets, global ETFs, or cross-market arbitrage. When the market opens, those adjustments are already embedded in prices.

All of these mechanisms push price discovery into the overnight window.

The Reality for Intraday Traders

None of this means intraday trading is impossible. Skilled traders do extract alpha within the trading session. However, the data highlights an important base rate: historically, the structural edge of the index itself appears to favor holding exposure overnight rather than trading within the day.

Intraday traders also face additional challenges. Transaction costs, slippage, and noise can erode performance, while the constant decision-making required during the trading session increases the likelihood of behavioral mistakes. When the aggregate intraday component of market returns is already small, these frictions make the hurdle even higher.

In contrast, long-term investors who simply maintained exposure overnight captured the majority of the market’s compounding.

The Risk of the Night

Of course, overnight exposure is not risk-free. Markets can gap dramatically due to earnings surprises, geopolitical shocks, central bank decisions, or global macro developments. Retail traders generally cannot hedge these risks perfectly.

One explanation for the overnight premium is that investors demand compensation for bearing this uncertainty. In other words, markets may reward those willing to hold risk while information continues to accumulate outside trading hours.

This trade-off between risk and return is part of what makes the anomaly persistent.

What This Data Really Tells Us

The broader lesson from this analysis is not that intraday trading should disappear or that overnight exposure is always superior. Instead, it highlights how different the actual mechanics of market returns can be from the way traders intuitively think about them.

Many participants spend years trying to optimize their activity during the six hours of the trading session. Yet over the past 26 years, the majority of the market’s long-term compounding occurred during the hours when the market was closed.

Sometimes the hardest truth in markets is that activity and value creation are not the same thing.

The market does not necessarily reward the hours you spend watching it.

Often, it rewards the patience to hold through the hours when no one is watching at all.